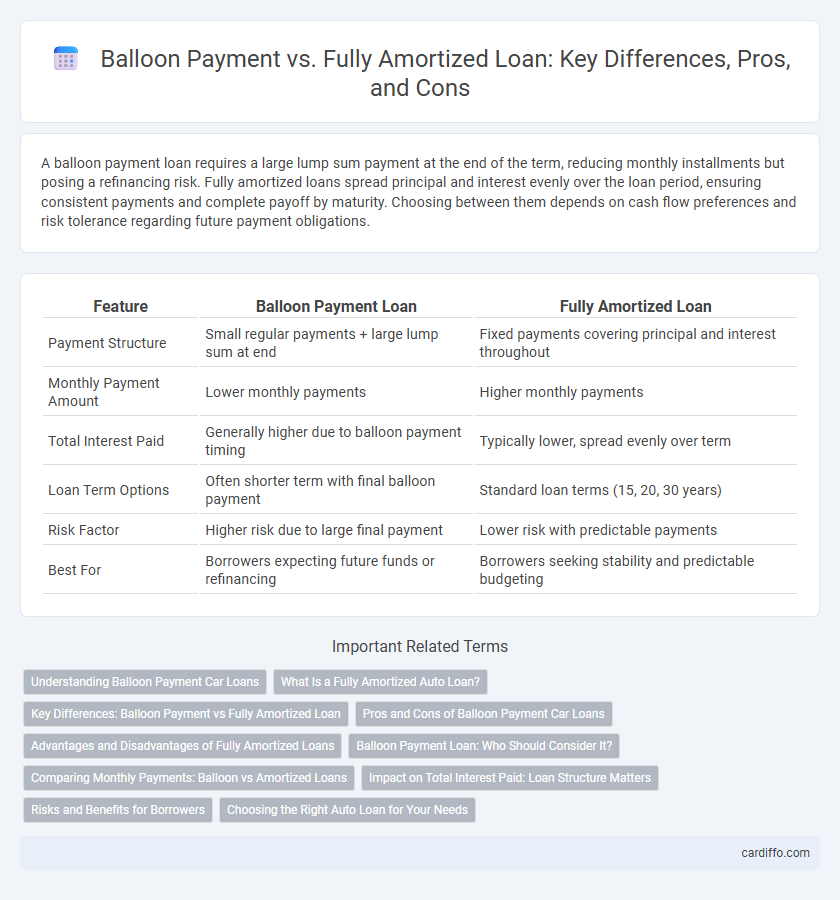

A balloon payment loan requires a large lump sum payment at the end of the term, reducing monthly installments but posing a refinancing risk. Fully amortized loans spread principal and interest evenly over the loan period, ensuring consistent payments and complete payoff by maturity. Choosing between them depends on cash flow preferences and risk tolerance regarding future payment obligations.

Table of Comparison

| Feature | Balloon Payment Loan | Fully Amortized Loan |

|---|---|---|

| Payment Structure | Small regular payments + large lump sum at end | Fixed payments covering principal and interest throughout |

| Monthly Payment Amount | Lower monthly payments | Higher monthly payments |

| Total Interest Paid | Generally higher due to balloon payment timing | Typically lower, spread evenly over term |

| Loan Term Options | Often shorter term with final balloon payment | Standard loan terms (15, 20, 30 years) |

| Risk Factor | Higher risk due to large final payment | Lower risk with predictable payments |

| Best For | Borrowers expecting future funds or refinancing | Borrowers seeking stability and predictable budgeting |

Understanding Balloon Payment Car Loans

Balloon payment car loans feature lower monthly payments with a large lump sum due at the end of the term, making them appealing for short-term financing but risky if the borrower cannot cover the final payment. Fully amortized loans spread payments evenly over the loan period, ensuring the car is paid off in full by the last installment, reducing the risk of unexpected expenses. Understanding balloon payment structures is crucial for borrowers to avoid financial strain and plan for the sizable end-of-term balance when financing a vehicle.

What Is a Fully Amortized Auto Loan?

A fully amortized auto loan is a type of loan where the borrower makes fixed monthly payments that cover both principal and interest, resulting in the loan being completely paid off by the end of the term. Each payment reduces the loan balance, ensuring no large lump-sum payment is required at maturity, unlike balloon payments. This structure provides predictable budgeting and full ownership of the vehicle once the loan is fully repaid.

Key Differences: Balloon Payment vs Fully Amortized Loan

Balloon payment loans require a large, lump-sum payment at the end of the loan term, while fully amortized loans are designed so that monthly payments cover both interest and principal, resulting in a zero balance by maturity. Balloon loans often have lower monthly payments but pose the risk of refinancing or paying a substantial final amount, whereas fully amortized loans provide predictable payments and full loan payoff without a remaining balance. The key distinction lies in payment structure and risk, with balloon loans suited for borrowers expecting increased cash flow or refinancing options in the future.

Pros and Cons of Balloon Payment Car Loans

Balloon payment car loans offer lower monthly payments compared to fully amortized loans, making them attractive for buyers seeking short-term affordability. However, the large lump-sum payment due at the end can pose a financial risk if refinancing or selling the vehicle isn't feasible. This structure benefits borrowers with fluctuating income but requires careful planning to avoid default or negative equity.

Advantages and Disadvantages of Fully Amortized Loans

Fully amortized loans offer the advantage of predictable monthly payments that cover both principal and interest, eliminating the risk of a large outstanding balance at the end of the term. This structure facilitates easier budgeting and faster equity building compared to balloon loans, which require a substantial lump-sum payment. However, fully amortized loans generally have higher monthly payments than balloon loans, potentially reducing initial cash flow flexibility for borrowers.

Balloon Payment Loan: Who Should Consider It?

Balloon payment loans are ideal for borrowers expecting increased future income or planning to refinance before the balloon payment is due. These loans offer lower initial monthly payments compared to fully amortized loans, making them suitable for individuals with short-term financial goals or fluctuating cash flow. Borrowers should carefully assess their ability to cover the lump-sum payment at the end of the term to avoid refinancing risks or default.

Comparing Monthly Payments: Balloon vs Amortized Loans

Balloon loans typically feature lower monthly payments during the loan term because they amortize only a portion of the principal, leaving a large lump sum due at the end. Fully amortized loans require higher monthly payments that cover both principal and interest, ensuring the entire loan balance is paid off by the final installment. Borrowers seeking lower initial monthly payments may prefer balloon loans, while those aiming for predictable, equal payments usually opt for fully amortized loans.

Impact on Total Interest Paid: Loan Structure Matters

A balloon payment loan typically results in higher total interest paid compared to a fully amortized loan because the principal remains largely unpaid during the term, causing interest to accrue on a larger balance. Fully amortized loans distribute payments evenly across principal and interest, reducing the loan balance steadily and minimizing interest accumulation. Borrowers choosing between these structures must consider how the loan design influences the total interest expense over the loan's life.

Risks and Benefits for Borrowers

Balloon payments offer lower initial monthly installments but expose borrowers to significant risk at the loan's end, requiring a large lump sum repayment or refinancing under potentially unfavorable terms. Fully amortized loans ensure predictable payments throughout the loan term, reducing default risk and promoting steady equity buildup, though monthly payments are typically higher. Borrowers seeking short-term cash flow relief might prefer balloon loans, but those valuing stability and long-term financial planning benefit more from fully amortized loans.

Choosing the Right Auto Loan for Your Needs

A balloon payment loan offers lower initial monthly payments but requires a large lump sum at the end, making it suitable for borrowers expecting increased future income or planning to refinance. Fully amortized loans spread payments evenly over the loan term, ensuring the vehicle is fully paid off without surprises, ideal for those seeking predictable budgeting. Assess your financial stability, future income prospects, and risk tolerance to determine whether a balloon payment or fully amortized auto loan aligns best with your needs.

Balloon payment vs fully amortized loan Infographic