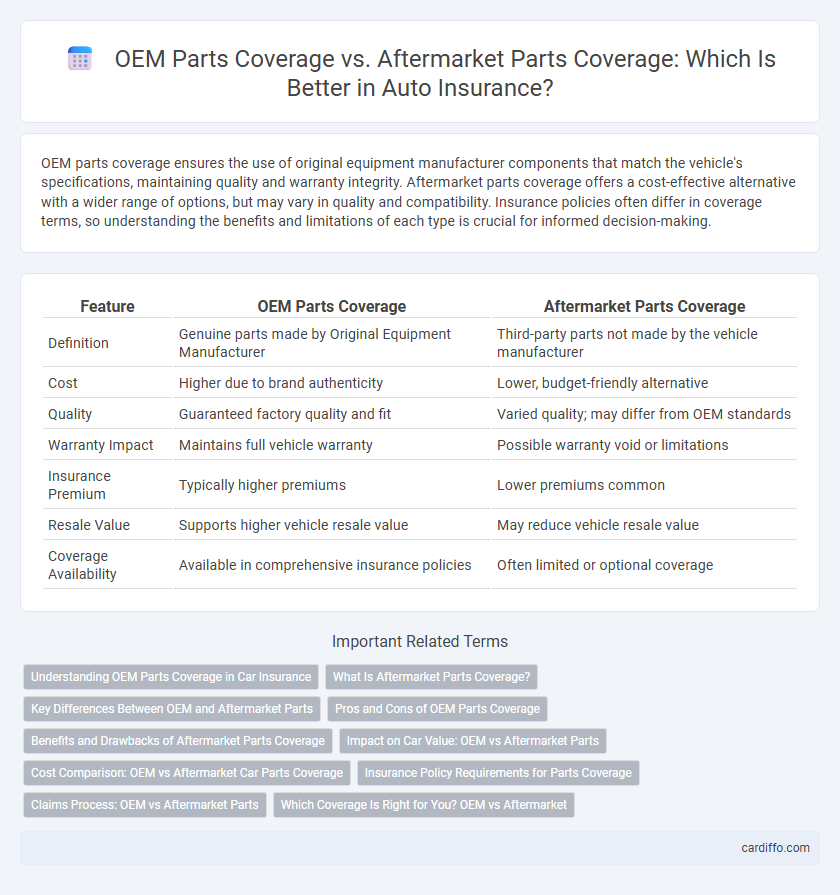

OEM parts coverage ensures the use of original equipment manufacturer components that match the vehicle's specifications, maintaining quality and warranty integrity. Aftermarket parts coverage offers a cost-effective alternative with a wider range of options, but may vary in quality and compatibility. Insurance policies often differ in coverage terms, so understanding the benefits and limitations of each type is crucial for informed decision-making.

Table of Comparison

| Feature | OEM Parts Coverage | Aftermarket Parts Coverage |

|---|---|---|

| Definition | Genuine parts made by Original Equipment Manufacturer | Third-party parts not made by the vehicle manufacturer |

| Cost | Higher due to brand authenticity | Lower, budget-friendly alternative |

| Quality | Guaranteed factory quality and fit | Varied quality; may differ from OEM standards |

| Warranty Impact | Maintains full vehicle warranty | Possible warranty void or limitations |

| Insurance Premium | Typically higher premiums | Lower premiums common |

| Resale Value | Supports higher vehicle resale value | May reduce vehicle resale value |

| Coverage Availability | Available in comprehensive insurance policies | Often limited or optional coverage |

Understanding OEM Parts Coverage in Car Insurance

OEM parts coverage in car insurance ensures that repairs use original equipment manufacturer parts, which maintain the vehicle's quality, performance, and resale value. Insurers providing OEM parts coverage often work directly with certified dealerships or authorized repair shops to guarantee authenticity and compatibility. This coverage typically costs more but offers superior protection compared to aftermarket parts, which may vary in quality and could impact vehicle safety.

What Is Aftermarket Parts Coverage?

Aftermarket parts coverage refers to insurance policies that cover the cost of non-OEM (Original Equipment Manufacturer) parts when repairing a vehicle after damage. These parts are produced by third-party manufacturers and are typically less expensive than OEM parts, providing a cost-saving option for policyholders. Insurers offering aftermarket parts coverage often balance affordability with quality standards to meet repair needs while reducing overall claim expenses.

Key Differences Between OEM and Aftermarket Parts

OEM parts coverage ensures the use of Original Equipment Manufacturer parts, which are identical to the components originally installed by the vehicle manufacturer, guaranteeing optimal fit and performance. Aftermarket parts coverage allows the use of third-party components that may vary in quality, cost, and compatibility, often resulting in significant savings but potential differences in durability. Insurance policies differ in how they authorize repairs, with OEM coverage generally leading to higher repair costs but maintaining factory standards, while aftermarket options provide budget-friendly alternatives with variable warranty and quality assurances.

Pros and Cons of OEM Parts Coverage

OEM parts coverage ensures the use of manufacturer-approved components, preserving vehicle integrity and maintaining warranty compliance. These parts offer guaranteed fit and quality but typically come at a higher cost, increasing repair expenses. While OEM coverage promotes long-term vehicle value and reliability, it may limit cost-saving opportunities compared to aftermarket alternatives.

Benefits and Drawbacks of Aftermarket Parts Coverage

Aftermarket parts coverage often reduces repair costs and insurance premiums by offering lower-priced components compared to OEM parts. However, these parts may vary in quality and durability, potentially affecting vehicle performance and resale value. Insurers may limit warranties on aftermarket parts, leading to increased long-term maintenance expenses.

Impact on Car Value: OEM vs Aftermarket Parts

OEM parts coverage preserves a vehicle's original quality and ensures alignment with manufacturer standards, directly supporting higher resale values and maintaining warranty compliance. Aftermarket parts coverage may lower repair costs but can lead to diminished car value due to potential mismatches in fit, finish, or performance, which buyers often perceive as less reliable. Insurers and appraisers typically favor vehicles repaired with OEM parts, reinforcing the importance of manufacturer-specified components in maintaining a car's market worth.

Cost Comparison: OEM vs Aftermarket Car Parts Coverage

OEM parts coverage typically incurs higher insurance costs due to the premium pricing of original manufacturer components, ensuring factory-quality repairs. Aftermarket parts coverage offers a more budget-friendly option with lower premiums, though it may involve non-original parts that could impact vehicle performance or resale value. Insurers often calculate premiums based on replacement part costs, making aftermarket coverage appealing for cost-conscious policyholders seeking affordable repairs.

Insurance Policy Requirements for Parts Coverage

Insurance policies covering automotive repairs often specify requirements for OEM parts coverage, mandating the use of Original Equipment Manufacturer components to ensure quality and maintain vehicle integrity. Aftermarket parts coverage policies allow non-OEM parts, typically at a lower cost, but may affect warranty and claims approvals. Understanding policy terms regarding parts coverage is essential to avoid disputes during claim settlements and to maintain compliance with insurer mandates.

Claims Process: OEM vs Aftermarket Parts

The claims process for OEM parts coverage typically involves direct coordination with authorized dealerships, ensuring precise fit and manufacturer-backed warranties that streamline repairs. Aftermarket parts coverage requires thorough verification of part quality and compatibility, potentially prolonging claim approval due to variable standards among suppliers. Insurers may impose specific documentation and inspection requirements for aftermarket parts to mitigate quality risks during the claims evaluation.

Which Coverage Is Right for You? OEM vs Aftermarket

Choosing between OEM parts coverage and aftermarket parts coverage depends on factors like vehicle value, budget, and repair quality preferences. OEM parts offer guaranteed compatibility and original manufacturer standards, ensuring optimal performance and maintaining vehicle warranty, while aftermarket parts provide a cost-effective alternative with variable quality and fit. Assess your insurance policy details and long-term vehicle maintenance goals to determine if the premium for OEM parts coverage aligns with your needs or if aftermarket options suffice for routine repairs.

OEM Parts Coverage vs Aftermarket Parts Coverage Infographic